Key Takeaways

- Most drivers in Ghana only understand insurance as a police requirement, not actual protection.

- Third-party insurance protects others, not your own car.

- Comprehensive insurance offers broader protection but still has strict conditions.

- Many claims are denied due to avoidable mistakes like late reporting or policy misuse.

- Knowing what to do immediately after an accident can determine whether your claim is approved.

Car Insurance Ghana: What It Covers (And What It Doesn’t)

For many drivers in Ghana, car insurance is something you get to avoid being stopped by the police. But the moment an accident happens, that assumption starts to break down.

To make sense of what insurance actually covers in Ghana, we spoke with an insurance professional at Enterprise Insurance. What exactly does your insurance cover? What are you actually protected against? And more importantly, what are you not?

Understanding this before you need it can save you from unexpected costs, rejected claims, and avoidable stress.

Check Out How Car Insurance Works When Renting a Vehicle With Us Here!

What Car Insurance Means in Ghana (Beyond the Paper Requirement)

In Ghana, motor insurance is not optional. To register and legally operate a vehicle, you must have at least Motor Third-Party Insurance, enforced by the DVLA and regulated by the National Insurance Commission.

But here’s where the misunderstanding starts: Many drivers see insurance as a formality, something to show authorities, not something to rely on. That mindset is risky. Because insurance is not just about compliance. It is about financial protection when things go wrong. And things do go wrong, especially on busy roads, highways, and during long-distance travel.

What Third-Party Insurance Covers (And What It Doesn’t)

Third-party insurance is the most basic and most misunderstood type of coverage.

What it covers

- Injury or death of other people involved in an accident

- Damage to another person’s property (vehicles, buildings, etc.)

- Passengers (if legally carried)

What it does NOT cover

- Damage to your own vehicle

- Your own medical expenses

- Theft or fire affecting your car

- Any damage beyond the policy limit

There is also a limit on how much can be paid out.

For example, property damage under basic third-party insurance is typically capped at around GH¢8,000, after which you cover the rest yourself.

This is where many drivers are caught off guard.

You may assume you are “insured,” but in reality, your protection is limited and often not enough.

Read More On The Best Car to Rent: SUV vs Sedan

What Comprehensive Insurance Covers

Comprehensive insurance offers broader protection, but it is not unlimited.

What it typically includes

- Damage to your own vehicle from accidents

- Theft or attempted theft

- Fire damage

- Natural disasters (floods, storms, riots)

- Windscreen damage

- Personal accident cover for driver and occupants

- Optional add-ons like towing or replacement vehicles depending on insurer

On paper, this looks like full protection. But here’s the part most drivers overlook:

When comprehensive claims are rejected

- Driving under the influence

- Using the vehicle outside its declared purpose (for example, commercial use for a private car policy)

- Allowing an unlicensed driver to operate the vehicle

- Policy not active or premiums unpaid

- Providing false or incomplete information

So even with comprehensive insurance, coverage depends heavily on your behaviour and compliance.

Get To Know More On How To Rent Out Your Car in Ghana: Obaa Akosua’s WopeCar Story

What Insurance Does NOT Cover (Even If You Think It Should)

- Mechanical breakdown or wear and tear

- Tyre bursts without an accident

- Full replacement value without depreciation

- Personal items stolen from the car

- Repairs done before insurer inspection

- Engine damage from flooding (unless specifically included)

These gaps are often the difference between a successful claim and paying out of pocket.

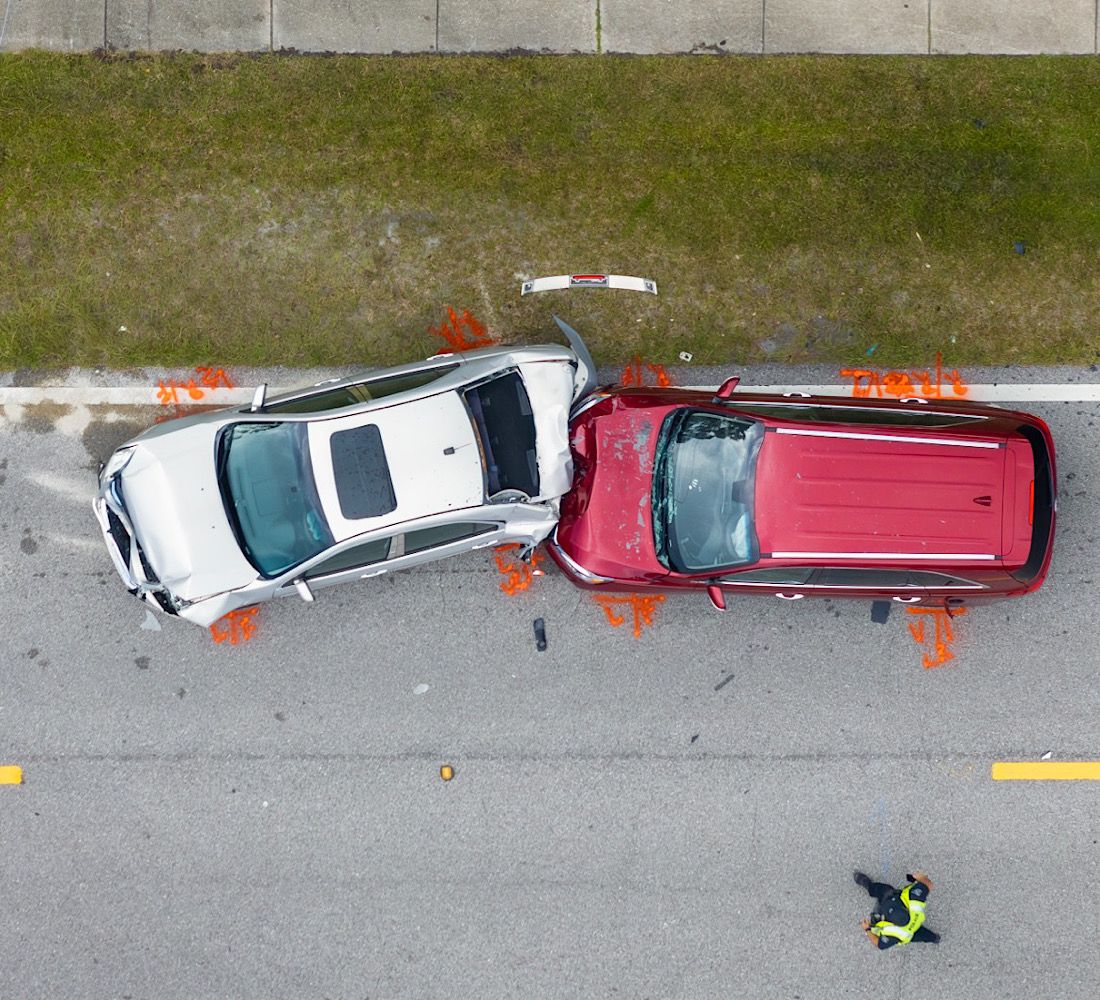

What To Do Immediately After a Car Accident

What you do in the first few hours after an accident can determine whether your claim is accepted or denied.

Step-by-step

- Ensure safety first. Check for injuries

- Report the incident to the police

- Obtain a police report

- Notify your insurer immediately (usually within 24–48 hours)

- Do not admit liability or settle privately

- Allow inspection by your insurer or loss adjuster

- Submit required documents (license, roadworthy, claim form, police report)

- Wait for assessment and approval

One of the most common reasons claims are denied is simple: Late reporting or incomplete documentation.

The Biggest Misconception Drivers Have

The most widespread misconception is that insurance exists mainly to avoid police trouble, rather than as protection in accidents. Most drivers are of the view that Insurance companies are only in for the money and not to pay claims and as such they only take insurance policies to avoid being stopped by the police.

Final Thoughts: Drive With Clarity, Not Assumptions

Insurance is not just a document. It is a system with rules, limits, and conditions. Understanding those details, before you need them, puts you in control. Because when an accident happens, you don’t want to be figuring it out in real time.